If you've owned a home over the past decade, chances are you've built far more wealth than you expected.

The last ten years have been unlike anything we've seen in modern real estate history. Homeowners experienced record appreciation, historically low mortgage rates, a global pandemic, inventory shortages, and one of the fastest shifts in housing demand ever recorded.

So the question everyone asks is:

Can it happen again?

The answer is yes—but probably not in the same way.

Looking Back: A Historic Decade

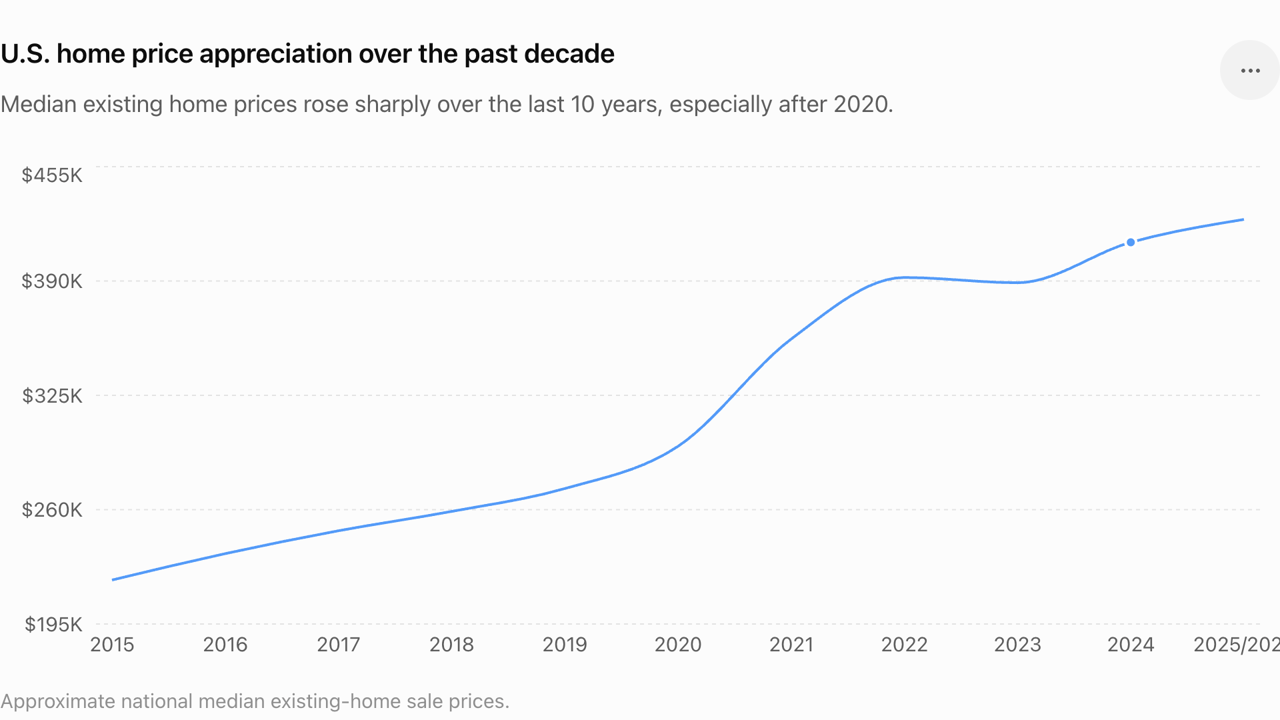

In 2015, the median existing home in the United States sold for roughly $220,000.

Today, that same median home is worth approximately $425,000, representing an increase of nearly 93% over ten years. That's equivalent to an average annual appreciation rate of approximately 6.8%—well above the long-term historical average of about 4% to 5%.

To put that into perspective:

- A $300,000 home purchased in 2015 would be worth roughly $575,000 today if it appreciated at the national average.

- That represents about $275,000 in equity growth, before considering any mortgage principal that was paid down.

For many American families, their home became their largest wealth-building asset.

Why Did Prices Rise So Much?

Several factors combined to create the perfect environment for appreciation.

1. America Didn't Build Enough Homes

For more than a decade after the housing crash of 2008, builders simply couldn't keep up with demand.

Millions of homes that should have been built never were. Even today, economists estimate the United States still faces a significant housing shortage.

When demand exceeds supply, prices naturally rise.

2. Mortgage Rates Reached Historic Lows

During 2020 and 2021, mortgage rates dropped below 3%.

That dramatically increased purchasing power.

Instead of buyers shopping for a $300,000 home, many suddenly qualified for $400,000 or more.

More buying power meant higher home prices.

3. Millennials Entered Their Prime Buying Years

America's largest generation entered the stage of life where people traditionally purchase homes, start families, and seek more space.

This demographic shift created enormous demand that continues today.

4. Homeowners Stopped Selling

Millions of homeowners refinanced into mortgages between 2% and 3%.

Now many are reluctant to sell because replacing that loan could double their interest rate.

This "lock-in effect" continues to limit inventory and supports home values in many markets.

Are We in Another Housing Bubble?

Many people compare today's market to 2008.

The data suggests they're very different.

Before the financial crisis:

- Lending standards were loose.

- Many buyers had little or no equity.

- Adjustable-rate mortgages were common.

- Builders were overproducing homes.

Today's market looks different:

- Lending standards remain much stronger.

- Most homeowners have substantial equity.

- Foreclosure rates remain relatively low.

- Housing inventory is still below historical norms in many areas.

That doesn't mean every market will appreciate every year, but it does mean the underlying fundamentals are healthier than they were before the last crash.

What Happens Over the Next 10 Years?

No one can predict the future with certainty.

However, history and current market fundamentals provide some strong clues.

Appreciation Will Likely Continue—Just at a More Normal Pace

The nearly 100% appreciation of the past decade was extraordinary.

Expecting that again would be unrealistic.

Instead, many economists anticipate long-term appreciation returning closer to historical norms, generally in the 3% to 5% annual range, though individual markets will vary significantly. Near-term forecasts also point to more modest price growth as higher mortgage rates temper demand.

Here's what that could mean:

Annual Appreciation | $500,000 Home Value After 10 Years |

|---|---|

3% | $672,000 |

4% | $740,000 |

5% | $814,000 |

Even "normal" appreciation can create hundreds of thousands of dollars in wealth over time.

The Markets That Will Win

National headlines often make it sound like every housing market moves together.

They don't.

Over the next decade, local factors will matter more than ever:

- Job growth

- Population growth

- Limited land for development

- Strong school systems

- Quality of life

- Infrastructure improvements

Communities that continue attracting residents and employers will likely outperform the national average.

My Perspective

I've watched buyers try to "time the market" for years.

Some waited because prices were too high.

Others waited because rates were too high.

Many eventually purchased the same type of home—only years later and at a much higher price.

No one consistently times the market.

The people who build the most wealth usually do something much simpler:

They buy when they're financially ready.

Then they stay invested.

Real estate has never been about finding the perfect year.

It's about giving appreciation enough time to work.

Final Thoughts

The last decade was exceptional.

The next decade probably won't produce another 90% jump nationwide—but that's not bad news.

A healthy housing market doesn't require explosive appreciation.

Steady growth, combined with paying down your mortgage, continues to make homeownership one of the most effective long-term wealth-building strategies available.

The market will change.

Interest rates will change.

Headlines will change.

But one principle has remained remarkably consistent throughout modern history:

Time in the market has almost always been more valuable than trying to perfectly time the market.

This article is provided for informational and educational purposes only and should not be considered financial, legal, tax, or investment advice. Real estate markets vary by location, and future appreciation cannot be guaranteed. The opinions expressed are based on historical market data and current economic conditions, which are subject to change. Buyers and sellers should consult with qualified financial, legal, and tax professionals before making real estate decisions. As a licensed real estate professional, I provide market insights but cannot guarantee future market performance or investment returns.